IFRS 17 as a Smart Insurance Solution

The digitization of all necessary areas of life has become an integral part of the past decade. Not surprisingly, technological solutions are constantly being optimized and improved through digitization. Being an integral part of all spheres of life and IT, in particular, the insurance software developers actively implements software in their systems. That is why the owners of insurance companies, web brokers, and other agents associated with the field of insurance are actively developing new ways to ensure and provide insurance for software developers.

The Internet requires instant access to a lot of data, and customers are used to completing instant purchases and ordering services with the help of insurance development services. All this, as well as the American law on recovery and reinvestment, called for a number of areas requiring rapid changes. Instant and effective solutions are impossible without first-class applications for insurance software development. Any competent insurance company adheres to a holistic approach to risk management and interested in insurance for app developers as well. As insurance companies increasingly turn to IFRS 17 as a smart solution, they must also find Android developers, eCommerce developer, and SAP ERP consulting experts to help them implement the necessary systems and tools.

A quick and effective risk management system and the prevention of potential business risks is essential for any insurance agency development. Moreover, this insurance software development sector has to be extremely credible and provide the 100% safety of its customers. A responsive software system with a number of good feedback builds an image of a reliable and transparent company. Therefore, experts in insurance software, solutions, and consulting experience a high market demand and gain a competitive advantage.

Such specialists should be able to find and develop new effective methods and tools for optimizing the operational processes associated with insurance policies, claims, and communications on B2B and B2C levels. The introduction of new IT insurance product development allows companies to increase loyalty and reduce their costs. In this article, we will talk about IFRS 17, the latest requirements for insurance for website developers and why you need to adhere to it today.

What Is IFRS 17?

When talking about what is IFRS 17, it is important to take into account that there are features of the work and development of insurance software for different regions. For example, in Europe, where insurers do businesses in accordance with high-quality standards for financial reporting, the international financial reporting standards were brought to the attention.

IFRS 17 stands for insurance contracts that were developed and implemented by an extensive group of insurers working on the development of IAS 17 under the control and coordination of the European Financial Reporting Advisory Group (EFRAG). They provide all the information about innovations, the impact of international financial reporting standard adoption, project implementation, and other updates about IFRS 17.

Since digitization has resulted in the need for standardization and organization to improve accountability in the field of operation and implementation of insurance, EFRAG identified 6 of the 11 main areas needed for optimization and improvement and the associations outside Europe aimed to revise the standard. Since October 2018, the forum of financial directors in Europe has been providing solutions for these 11 problem areas.

It is worth noting that the contracts complying with IFRS 17 are built on the principles for identifying, evaluating, and disclosing information according to the adhered standard. The purpose of IFRS 17 is to ensure that the developers’ insurance company provides relevant information that truly represents such contracts. This information contains the basic points needed for reliable financial statements that influence further insurance contracts, the financial position of employees, financial results of the company, and revenues of the organization.

When applying IFRS IAS 17, an organization must take into account its actual rights and obligations, regardless of whether they are stipulated in the contract, law, or regulation. Contracts may be written, oral, or agreed with any company’s usual business practices, and the legal protection of rights and obligations in the agreement is ensured by law. Contractual terms include all expressed or implied terms, but the organization should not take into consideration the conditions that do not have a commercial content (that said, some conditions may not have a noticeable effect on the economic side of the contract but still are important to specify). Implied terms of the contract include those required by law or regulatory requirements. The practice and procedures for concluding contracts with customers vary by jurisdiction, industry, and organization. In addition, these may differ within the same organization (for example, procedures may depend on the category of customers or the nature of the promised goods or services).

IFRS 17 allows companies to see financial statements from a completely different perspective because of the approaches used by analysts to interpret the results and compare companies around the world constantly change. At the moment, the new standard provides equal conditions for insurers reporting under IFRS, disclosing the contents of the “black box” of the current accounting for insurance contracts. The new IFRS 17 standard brings insurers both benefits and problems, and they need to figure out how to change the accounting procedure and the corresponding impact on the businesses.

Below you can find the basic principles that define the insurance policy for IFRS 17:

- An insurance contract provided by a company or an organization is a contract in which the organization undertakes to pay compensation to the policyholder for risk or unfriendly event that bears a significant loss or adversely affects it.

- IFRS 17 separates the insurance contract from all other types of services and goods that are not related to the insurance field, as well as divides tools and investment components.

- All contracts are determined by separate groups, which have their own number of features and peculiarities.

Groups of insurance contracts can be divided by the following categories:

- The one presenting the forecast for future revenues, including own profits, and delivering detailed information on the accessing cash flows, unearned profits, and the pre-service margin

- The one recognizing the profit from the insurance group during the period of the contract, as well as from a risk-free enterprise with insurance coverage

- The one providing information on insurance incomes, expenses, and other financial insurance services

- The one under IAS 17, evaluating the financial influence of a contract on the revenue result and cash flow of the company.

How Can Insurance Software Development Help to Protect Business?

Any website developer working with software for insurance companies knows that their business is always at risk every time they communicate with a client or public. The ideal solution for insuring businesses and protecting against financial consequences and unforeseen disasters is an individual insurance solution.

To protect the results of their work, the programmer of any specialty must have business insurance. If you contact an independent insurance agent, you will get an offer for an insurance software development solution with the types of insurance that will suit your case.

There are four types of software development insurance for developers, and you can find a description for each of it below:

- Commercial General Liability Insurance (CGL)

This type of insurance provides you with protection against claims of the client for compensation for material damage. If, for example, the client states that your employees have damaged some equipment during work, your insurance can pay for the loss. Similarly, this type of insurance for web developers covers minor medical expenses related to your employees.

Such policy of shared responsibility also works great in protecting your business insurance software developers from intellectual property claims (images, code, and other copyright property).

- Commercial Real Estate Insurance

This web development insurance includes protection against damage to the leased building and its contents (equipment, furniture, consumables). Damage caused by fire, theft, or vandalism will be covered in case you insure your leased real estate. Also, optionally, you can insure against business interruption due to relocation or loss of property.

- VOR Business Owner Policy

Small businesses have the right to a comprehensive VOR policy, which includes general developers’ insurance company responsibilities, as well as property and business breaks at an affordable price. Your independent provider can help you to determine if you can save on an insurance product development software by purchasing a business owner’s policy.

- Professional Liability Insurance of Errors and Omissions Coverage (E&O)

This type of insurance created for insurance companies software developers protects your programmers from professional errors affecting the financial condition of the client. A claim for damage may be caused if such errors were made as failure to complete the project on time because the coding errors can significantly affect downtime and failures leading to system vulnerability. Since mistakes can always occur, this type of insurance development services protects against such claims that are not covered by the general policy. If you do not have suitable professional responsibility insurance, your assets are in danger.

What Is the Novelty of IFRS 17 for Insurance Development Services?

Increasing the transparency of information on the profitability of a business, whether new or existing, enables businesses to assess the financial stability of the insurer more deeply than ever before. Here are the benefits guaranteed by IFRS 17 implementation for any type of business:

- Separate presentation of underwriting results and financial revenues results in greater transparency with respect to sources of profits and the quality characteristics of the reported profits.

- The main components of the insurance contract no longer depend on the insurance package, since the investment components and the resulting costs are no longer considered revenue.

- The treatment of options and guarantees will become more consistent and transparent.

A potential consequence of these factors for leading insurance website development companies may result in a reduction of the capital cost. On the other hand, higher comparability of the reported data stimulates growth in mergers and acquisitions, increases competition for investment capital, and helps to win investor confidence. Other consequences include a tracked volatility of financial results and revenues that can boost as a result of utilizing up-to-date market solutions as discount rates. Usually, insurers firstly review their company’s structure and its distribution of investments to offer the best insurance option.

What Do You Need to Know about IFRS IAS 17 Leases?

It is also important to understand how the accounting policy is maintained between the landlord and tenant, which is governed by IFRS IAS 17 leases, as is the disclosure to both parties. IFRS (IAS) 17 leases payments are recorded throughout the entire term of the operating lease, evenly throughout the entire contract period. This can be changed only if another system for temporary distribution becomes more profitable for the user. Regarding finance leases, tenants must recognize finance leases as specific liabilities and assets that they maintain in the financial statement for amounts equal to or less than the value of the minimum lease payment at the beginning of the transaction.

Differences in the approach to accounting for rent under IFRS IAS 17 leases do not allow investors and other users of financial statements to compare companies because they have to proceed with off-balance-sheet accounting for operating leases themselves. For every insurance agency website development comes with a number of recognized assets and significant liabilities on financial performance. In return, many accounting requirements for tenants have been changed.

IFRS 16 works to annual results starting from January 1, 2019. Early application is permitted if the company uses in IFRS 15, “Revenue from contracts with customers.” IFRS 16, in contrast to IAS 17, did not allow a tenant to classify a lease in two ways – as operating or as financial. Consequently, the financial statements of tenants were affected the most, and this was due to an increase in recognized lease assets and financial liabilities.

It is worth noting that the accounting for leases under the new IFRS 17 standard will be similar to the IFRS 16, with some exceptions, allowing the client not to record assets and liabilities on the balance sheet in the causes below:

- a short-term lease (not more than one year, with possible extension);

- lease of low-value assets (for example, personal computers, telephones, office furniture, but not autos).

The lease term is defined as a non-contracted period during which the tenant has the right to use the asset under the contract, along with the timing, including the possibility (paragraph 18, IFRS 16):

- Of a lease renewal if the tenant has reasonable confidence that he will take advantage of this opportunity;

- That a waiver of the tenant has a reasonable assurance that he will not take advantage of this opportunity.

The above exceptions do not oblige the tenant to use them. At will, he can account for these assets in full compliance with IFRS 16, namely as a financial lease.

Vital Points to Take While Considering Insurance Agency Development

We recommend companies to start preparing for the entry into force of IFRS 17 right now. To assess the potential impact of it, insurance agency development should:

- negotiate with the bank providing financing to the company, and if financing agreements depend on ratios that will be significantly changed as a result of accounting for rent on the balance sheet, discuss the implications for financing agreements (such factors may include financial leverage ratio characterizing the ratio of equity and debt, interest rate, EBITDA, etc.);

- conduct appropriate preliminary preparations of insurance agency development to assess the impact of leases on the future balance, including the effects of existing leases and those that are under discussion;

- collect comparable data on lease agreements accounted for in accordance with IAS 17 vs IFRS 17, which will be effective after the effective date of IFRS 16;

- assess the need for an IFRS 16 transition expert and the acquisition of appropriate rental accounting software.

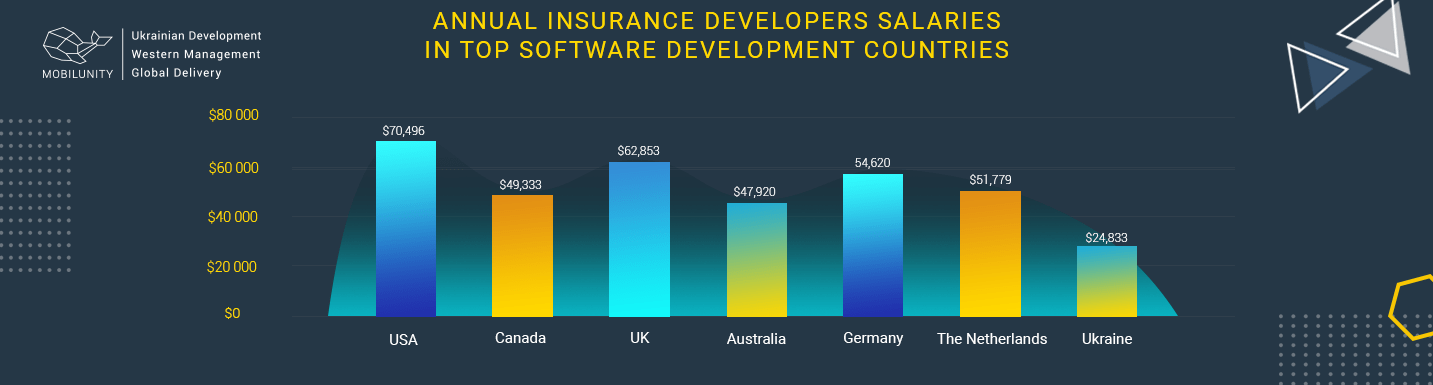

According to Statista, last year only the insurance companies in the US spent more than $82 billion dollars on insurance software development. There are more and more insurance software development companies entering the market and conquering for leading positions. While there is much in-house software development held in the US, delegated and outsourced development gets to be even more useful for businesses. Let’s take a look at insurance development cost services in top software development countries to consider:

- The US – $70,496

- The UK – £50,289 ($62,853)

- Canada – C$64,780 ($49,333)

- Australia – AU$68,659 ($47,920)

- Germany – €49,021 ($54,620)

- The Netherlands – €46,463 ($51,779)

- Ukraine – $24,833

As you can see, among the most reputable countries for insurance software development, Ukraine offers the lowest rates. It is not because of the low-quality approaches; exactly the opposite, Ukrainian companies are in high demand because of the optimal correlation between the development costs and the insurance solutions. If you are looking for a reliable software development company to outsource your insurance product development, Ukrainian specialists can be a great match for your business needs.

Why Choose Mobilunity as Your IFRS 17 vs. IAS 17 Implementation Partner?

If you need information for your insurance software engineer, developer, or designer, you can get professional help from local insurance agents at Mobilunity. Here you can find a great number of professional mobile app developers for insurance and dedicated managers for your specific needs. As a reliable IFRS 17 implementation partner, we are eager to help you make the right decision and choose the best offer for your insurance development services, as well as create a policy that suits your specific needs. Minimize the risks to your business and get insurance for web developers or professional advice from Mobilunity experts today!

If you are looking for expert assistance in implementing IFRS 17 standards in your business, you are welcome to contact Mobilunity specialists. Get professional help right now!

All salaries and prices mentioned within the article are approximate NET numbers based on the research done by our in-house Recruitment Team. Please use these numbers as a guide for comparison purposes only and feel free to use the contact form to inquire on the specific cost of the talent according to your vacancy requirements and chosen model of engagement.